1.0 Introduction

Over the past two decades, global concern has intensified regarding the threat of money laundering, particularly its evolving relationship with financial technology (FinTech). The International Monetary Fund (IMF) has identified money laundering as a systemic threat that undermines financial stability, fosters illicit financial flows, and erodes trust in cross-border capital mobility (IMF, 2022). While FinTech innovations have enhanced financial inclusion, efficiency, and customer experiences, they have also created new vulnerabilities that money launderers exploit. Emerging technologies such as blockchain, cryptocurrencies, mobile money, and peer-to-peer (P2P) payment systems offer anonymity, speed, and cross-border capabilities, challenging the efficacy of traditional Anti-Money Laundering and Counter-Financing of Terrorism (AML/CFT) controls (Alexandre & da Silva, 2023; Tertychnyi et al., 2022).

The intersection of FinTech and money laundering is not just a theoretical concern but a practical regulatory dilemma. Recent developments show that while FinTech can aid AML efforts through RegTech innovations and AI-powered monitoring tools (Jensen & Iosifidis, 2023), it can equally obscure financial trails, making detection and enforcement more complex. This dual nature demands a deeper investigation into the regulatory blind spots, especially in developing economies like Nigeria, where FinTech adoption is rapidly increasing without commensurate regulatory evolution. According to GIABA (2020), West Africa remains highly susceptible to FinTech-facilitated money laundering due to weak legal frameworks and limited cross-border cooperation.

This study is driven by three critical gaps in the current body of knowledge. Firstly, there is a dearth of empirical research specifically examining the nexus between FinTech innovation and money laundering exposure from the perspective of regulators. Most existing studies are either fragmented, outdated, or overly general, lacking context-specific insights particularly relevant to emerging economies. Secondly, the methodological landscape of prior research is limited, often skewed toward descriptive or case-based approaches that fail to capture the nuanced and evolving nature of FinTech-facilitated money laundering (Ali, 2019; Isaac, 2018). Thirdly, and most importantly, the regulatory viewpoint remains significantly underrepresented, despite the fact that regulators play a central role in designing, operationalizing, and enforcing AML/CFT controls. The need to explore these gaps has become more urgent with the rapid adoption of decentralized finance (DeFi), virtual assets, and real-time digital payment systems technologies that often outpace traditional regulatory mechanisms (Pratama et al., 2024; Suherman, Nasir & Utama, 2025).

In response, this study delivers actionable insights into how regulatory authorities perceive and respond to the increasingly complex threats posed by FinTech within AML/CFT frameworks. As digital financial services expand in scope and reach, the study aims to improve regulatory preparedness by informing the creation of adaptive, technology-responsive laws. These insights are especially valuable for jurisdictions grappling with the dual challenge of encouraging financial innovation while safeguarding financial system integrity. The study highlights the importance of equipping regulators with the necessary institutional, technical, and legal tools to anticipate and counter emerging financial crime risks in a rapidly digitizing economy.

The findings are expected to strengthen international cooperation and support capacity-building initiatives within AML/CFT regimes, particularly across developing economies. For policymakers, the study will offer timely input to guide the development of future FinTech policies in Nigeria and comparable jurisdictions, ensuring that innovation is not achieved at the cost of regulatory blind spots. Furthermore, the research will inform the ongoing development and adoption of regulatory technology (RegTech) solutions, which are critical for detecting, preventing, and mitigating money laundering risks associated with decentralized finance, digital currencies, and real-time payment systems.

Beyond its national context, the study contributes to the global AML/CFT literature by offering empirical, data-driven insights from Africa’s largest economy. In doing so, it aligns with the strategic priorities of global stakeholders such as the Financial Action Task Force (FATF), the Inter-Governmental Action Group against Money Laundering in West Africa (GIABA), and the International Monetary Fund (IMF), all of which have emphasized the importance of adapting financial governance to the unintended consequences of rapid FinTech proliferation (FATF, 2023; IMF, 2022).

By focusing on Nigeria’s regulatory institutions, this study fills a critical empirical and contextual gap in understanding how national regulators interpret, respond to, and seek to mitigate the complex interactions between FinTech and money laundering. It also extends the Technological Determinism Theory into the Anti-Money Laundering and Countering the Financing of Terrorism (AML/CFT) regulatory domain.

The study offers a deep-dive analysis of FinTech’s impact on money laundering exposure from the perspective of Nigerian regulatory authorities. The findings will be valuable to academics, financial regulators, international bodies, and practitioners aiming to balance financial innovation with systemic integrity.

The remainder of the paper is structured as follows: Section 2 reviews the relevant literature; Section 3 outlines the research methodology; Section 4 presents the results and discussion; and Section 5 concludes with key findings and policy implications.

2.0 Literature review

2.1 Conceptual Framework of Money Laundering

Money laundering is defined as the illicit process of deriving profit from financial transactions and concealing or utilizing the proceeds for criminal purposes (Odu, 2020). Terrorism financing involves raising, storing, and moving funds acquired through legal or illegal means to support terrorist acts or maintain the logistical structure of a terrorist organization (Stringer, 2011). Money laundering encompasses various activities like corruption, market manipulation, tax evasion, drug trafficking, and fraud, diverting resources from economic and social welfare to criminal endeavors. To combat these issues, the International Monetary Fund (IMF) has developed Anti-Money Laundering/Combating the Financing of Terrorism (AML/CFT) controls regularly assessed and updated to mitigate associated impacts (IMF, 2019).

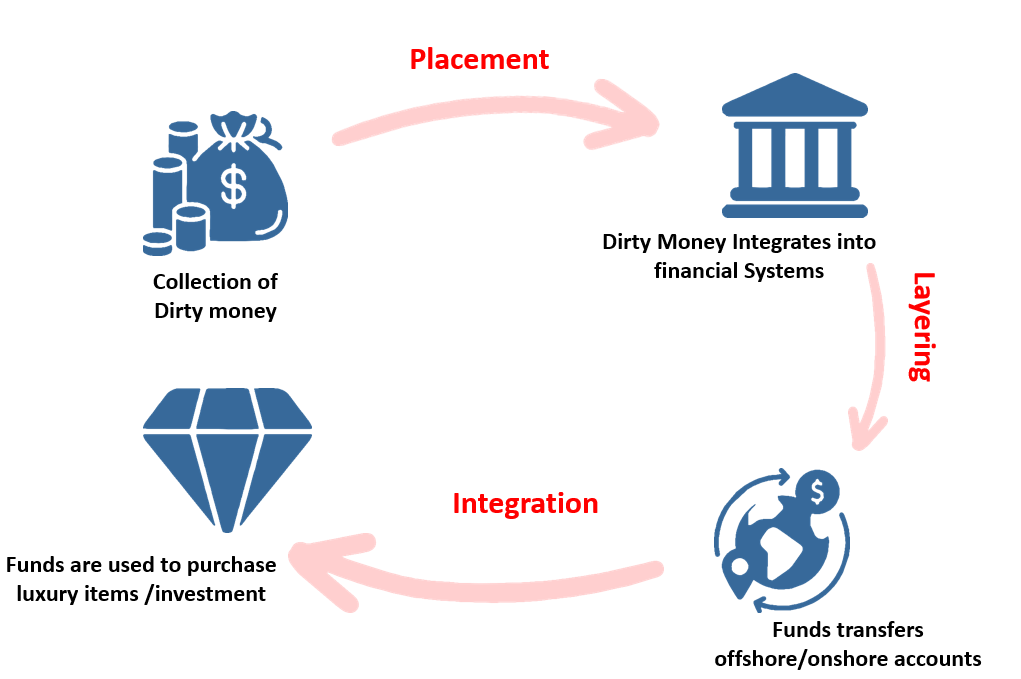

Money laundering process comprises three key stages: Placement, where illegally acquired funds enter the financial system, often in smaller, less suspicious sums; Layering, which obscures the audit trail through complex financial transactions, wire transfers, or the use of shell companies; and Integration, where "cleaned" money is reintroduced into the economy, appearing legitimate through investment in legal businesses or assets as illustrated in Figure 1. Various techniques, such as the use of shell companies, smurfing, trade-based laundering, and cryptocurrencies, are employed in the money laundering process (FCA, 2023)

Figure 1: Money laundering stages flow

Odu (2020) establishes a connection between money laundering and FinTech, suggesting that FinTech empowers unregulated markets, facilitating both legitimate and illicit transactions. While Phillips and McDermid (2020) argue against labeling digital financial products and services as havens for criminals, both studies acknowledge a potential link between FinTech and money laundering or terrorism financing.

Money laundering is a global issue affecting all economies, involving the movement of money through legitimate businesses to conceal crime, fraud, or trafficking. Ogbodo and Miseseigha (2013) describe it as concealing the source, nature, and disposition of illegally obtained money or property. Money laundering, essential for sponsoring crimes and disturbing societal peace, requires a structured financial institution. Ribadu (2004) notes that money laundering in Nigeria involves exchange houses, brokerage firms, trading organizations, car dealerships, and casinos. The Nigerian government implements policies and frameworks, including FATF Reports, GIABA Review, and the review of existing regulations, to counter money laundering and fraud (Enofe, Adijatu, Atombara, 2018).

2.1.1 Financial Action Task Force (FATF) Report

The Financial Action Task Force on Money Laundering captured in French as groupe d’action financiere (GAFI) established in France, is an organization formed by different government of the world and founded in 1989. This initiative developed by G7 summit is to maintain certain interest and combat money laundering. On incorporation, the FAFT was known only to combat fraud, however in 2001; the scope was widened to fighting Terrorism, terrorism financing and other related crime. The major objective of the FATF is to maintain, implement and set out procedure for the legal, regulatory and operational measures for combating and reducing the effect of money laundering, terrorism, terrorist financing and other related offences which distorts and threatens the international financial system. The FATF is a regulatory body known for developing and implementing policies that counter terrorism, and terrorist financing that is capable of disturbing world peace. This is because policies developed are reviewed by each member nation which makes it a mutual evaluation process, this system makes the policies and regulation to be very effective since expatriate are involved in its peer review process.

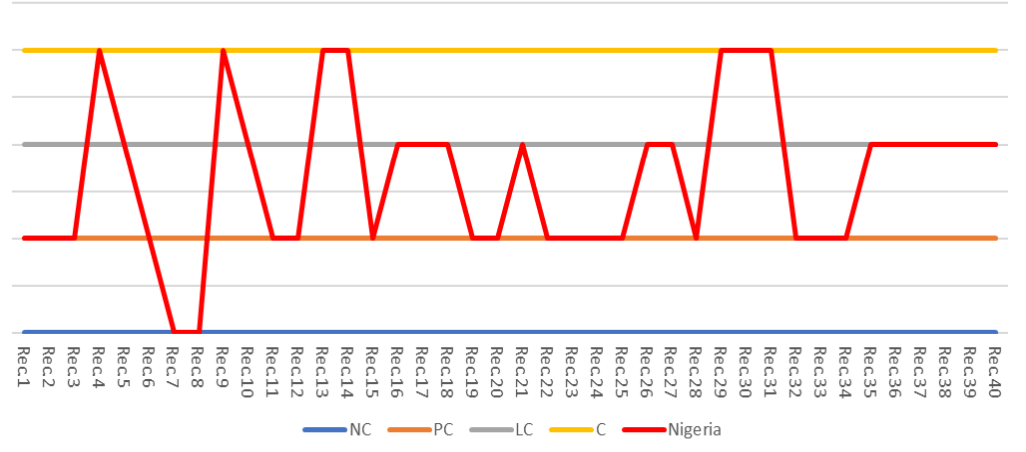

The mutual evaluation process helps to access the rate of compliance with the recommendations and strength of the AML/CFT process, in furtherance to this, ratings are given to countries on technical compliance based on recommendations. The FATF report in the Nigerian financial space has not been so palatable, Abiola (2013) remarked that Nigeria keeps featuring on the grey list of the Financial Action Task Force. She has not been fully committed in complying with the methodologies outlined by the FATF, for example, the Boko /ISWAP group case. The FATF reports reveal that Nigeria has little or no understanding of the causes and linkages of the menace. In 2021, the mutual evaluation reports relating to the implementation of anti-money laundering and counter terrorist financing standard was carried out in Nigeria, among other things, it was found that Nigeria was only compliant in 14 out of the 40 FATF core benchmark. This suggests the low compliance and implementation of the FATF methodologies.

Source: NFIU 2021

C (Compliant): No shortcomings

LC (Largely Compliant): Minor shortcomings

PC (Partially Compliant): Moderate shortcomings

NC (Non-Compliant): Major shortcomings

Figure 2: Nigeria’s Technical Compliance with FATF Recommendation

2.1.2 Inter Government Action Group against Money Laundering in Africa (GIABA) Report

Similar to the FATF, GIABA is a regional inter-governmental organization in Africa tasked with periodically reviewing methodologies and processes aimed at combating terrorism and money laundering activities. The GIABA report reveals that, most ML/TF risk in Nigeria is predicative. They submit that the most prevalent money laundry case in Nigeria is corruption, advanced fee fraud, trafficking, maritime offences, kidnapping and human trafficking. Corruption is endemic in the Nigerian economy and carried on domestically with majority of it proceed laundered abroad. On Terrorist Financing, Nigeria faces the deadliest group called Boko Haram, which have strong ties with world renowned ISIS.

This group poses a serious threat to the growth and development of Nigeria. They operate majorly in the northeast of Nigeria by engaging in nefarious activities such as kidnapping, robbery and taxation raiding in other to finance their activities. Since the conduct of the first evaluation carried out by GIABA in 2008, the Nigerian financial space has witnessed a tremendous turnaround in terms of AML/CFT framework which is in line with best standard (FAFT). To tackle this problem of AML/CFT, the Nigerian government has enacted some regulations, they comprise; the Money laundering prevention and prohibition Act (2022) which repealed the money laundering prohibition Act, 2011 (MLPA), The Nigerian Financial Intelligence Units Act, 2018 (NFIU), the Mutual Legal Assistance in Criminal Matters Act, 2019 (MLACMA) and the Terrorism Prevention Act (TPA).

Despite the establishment of a comprehensive Anti-Money Laundering and Counter-Financing of Terrorism (AML/CFT) framework, Nigeria continues to face significant challenges in effectively assessing and mitigating money laundering (ML) risks, particularly those associated with fraud and corruption. The Inter-Governmental Action Group against Money Laundering in West Africa (GIABA) has highlighted that Nigeria has not conducted a detailed examination of ML risks related to fraud and corruption, despite their substantial contribution to illicit financial flows in the region.

Furthermore, the 2024 GIABA Follow-Up Report indicates that Nigeria lacks clear strategies to address these ML risks comprehensively. The report also underscores the absence of a thorough assessment of vulnerabilities faced by persons with disabilities, who may be exploited for ML or terrorist financing purposes.

While supervisory bodies such as the Central Bank of Nigeria (CBN), the Securities and Exchange Commission (SEC), the National Insurance Commission (NAICOM), and the Special Control Unit Against Money Laundering (SCUML) have developed a general understanding of ML risks within their respective sectors, efforts to educate and guide reporting entities have not been sufficiently effective. This shortfall hampers the entities' ability to implement risk-based AML/CFT measures effectively.

In light of these deficiencies, GIABA recommends that Nigeria prioritize a comprehensive assessment of ML risks related to corruption, fraud, legal persons, and politically exposed persons (PEPs). Additionally, it is imperative for reporting entities to explicitly report any suspicious transactions associated with ML and its predicate offenses to enhance the effectiveness of the AML/CFT regime.

2.1.3 Extant Regulation on Money Laundering in Nigeria

Since its inception and implementation, the AML/CFT Act, specifically the Money Laundering Prevention and Prohibition Act (2022), which supersedes the Money Laundering Prohibition Act, 2011 (MLPA), has served as the primary existing regulation on money laundering until the establishment of the Nigerian Financial Intelligence Units Act. The objective of the Act is to provide for an effective and comprehensive legal institutional framework for the prevention, prohibition, detection, prosecution and punishment of money laundering and other related offences in Nigeria (Federal Republic of Nigeria Official Gazette on Money Laundering 2022). The regulation made a clear cut to which a financial institution should blow the whistle when cash deposit exceeding the limit provided has been made. A cap of five million naira or its equivalent in the case of an individual and ten million naira in case of corporate bodies is not to be exceeded. The Act provided for the establishment of a department under the EFCC called the Special Control Unit Against Money Laundering (SCUML).

The SCUML shall be responsible for the supervision of designated non-financial businesses and professionals in their compliance with the provision of the Act. The function of the SCUML is to register, monitor, enforce, inspect, and maintain a comprehensive database for non-financial business and profession. As at today, the SCUML has been moved as a department under the EFCC to a separate agency to allow for autonomy and full discharge of their duties. Also, Part five of the Act talks about offences and penalties of money laundering in Nigeria, offences listed include concealing or disguising the origin of, covert and transfers, removing from the jurisdiction and taking control of any fund or property reasonably known to be from an illegal or unlawful source. The provision forms the bedrock for the AML/CFT guidelines in Nigeria.

2.2 Financial Technology (FinTech)

FinTech refer to services rendered through mobile phones, personal computers and cards linked to dependable digital payment system facilitated by internet (Ozili, 2018). In a subsequent investigation and publication conducted by the Financial Stability Board, FinTech is defined as a technology-enabled innovation within the realm of financial services, capable of engendering novel business models, applications, processes, or products, thereby exerting a tangible impact on service provision (FSB 2023)." It operates using arrays of stakeholder groups covering banks/other financial institutions, mobile network operators, financial technology providers, regulators, agents, chains of retailers and clients (Michelle, 2016), which facilitates several financial services including agency banking, internet banking and mobile banking, and even student financial management (Suherman, Nasir & Utama, (2025). The main objective of business finance is to contribute towards efficient financial intermediation, financial stability and sustainable development (Ozili, 2021). In Nigeria, the country has been committed to the development of FinTech through National Financial Inclusion Strategy (NFIS) introduced in October 2012. This commitment is in relation to the four dimensions of FinTech including mobile-based financial services, web-based financial services, POS-based financial services and ATM-based financial services. These are discussed in the following sub-sections.

In Nigeria, the trajectory is also upward sticky. Digital finance sustained uptick from January 2009 when the Central Bank of Nigeria through moral suasion encouraged deposit money banks to deploy payment system infrastructure to reduce cash handing and cash-based transactions. Due to the suasion and deployment of FinTech regulations in Nigeria, transaction through digital platforms increased astronomically. For instance, ATM transactions increased by 1,412% to Naira638.07 billion in December 2018 from Naira42.20 in January 2009. Similarly, mobile banking, internet banking, and Point-of Sales (POS) increased astronomically within the period (Ujunwa et al. 2022).

2.3 Nexus between FinTech and Money Laundering

McLuhan's Technological Determinism Theory (1964) underscores the connection between FinTech and money laundering. However, empirical evidence in applying this theory to financial technology has only recently emerged, which is unsurprising given the evolving nature of FinTech as a research area. A notable study by Hariyono and Tjahjadi (2021) utilized the Technological Determinism Theory to examine the role of intellectual capital in the development of financial technology during the new normal period in Indonesia. Interestingly, the study found that intellectual capital, particularly human skills, did not significantly contribute to the development of financial technology in the current new normal context in Indonesia. Consequently, this study provides valuable insights into the application of the Technological Determinism Theory (McLuhan, 1964) as well as Legal, Economic, Technological” model and preventing transnational crimes (Pratama et al., 2024) within the realm of financial technologies.

Digital finance introduces distinctive challenges and risks due to the diverse supply channels, services, and products provided by service providers (Odu, 2020). Among these challenges is the potential for exploiting these channels to facilitate crimes such as money laundering. The development of FinTech in Nigeria corresponds with a decline in the country's ranking on the Basel Anti-Money Laundering Index, moving from the 16th most vulnerable country in 2012 to the 14th in 2019 (Basel Institute of Governance, 2012; Basel Institute of Governance, 2019). This suggests a potential association between the increased penetration of FinTech and a rise in money laundering. FinTech, particularly digital finance like FinTech, has empowered financial service providers in an ostensibly unregulated yet attractive market, facilitating both legitimate and illicit transactions (Odu, 2020).

The study of Campbell-Verduyn (2018) on Bitcoin, crypto-coins, and global anti-money laundering governance also underscores the link between FinTech and money laundering. The study evaluates the effectiveness of the global anti-money laundering regime in addressing challenges and opportunities presented by novel altcoins. It emphasizes the need for the FATF to strike an effective balance between existing threats and opportunities associated with crypto-coins, calling for continuous monitoring and investigation into the broader ethical implications raised by crypto-coins for global anti-money laundering efforts amidst rapid technological change.

While combating online crime has been a priority at national and international levels, studies by Tropina (2014), Bjelajac (2011), and Venkatesh et al. (2020) suggest that digital finance practices are linked to money laundering in both developed and developing nations. Bodescu, Achimb, and Rusc, (2022) using data for 162 countries in 2012-2020 time period through econometric methods and models, independent variables as percentage of individuals using internet and technology adoption found clear evidence for the entire sample that increase FinTech leads to decrease in the risk of money laundering. A more recent study found that FinTech development increase money laundering risks (Bhunia, et al., 2023).

3.0 Methodology

3.1 Research Design

The research designed deployed in this study is qualitative using interpretivist paradigm and the data was collected through interviews with regulators from FinTech and money laundering regulators within the Nigerian banking industry. It is important to note that in qualitative studies, the most common approaches are interview and observations (Jamshed, 2014). However, interview was selected as the study seek the views of the respondents not observing their behaviors. In this, key informant interview (KII) was conducted with the relevant staff of the six regulatory bodies which include Central Bank of Nigeria (CBN), Nigeria Financial Intelligence Unit (NFIU), Economic and Financial Crime Commission (EFCC), Independent Corrupt Practices and Other Related Offences Commission (ICPC), National Drugs Law Enforcement Agency (NDLEA) and the Ministry of Justice. The collection of data collected was cross-sectional, the data was collected at one-point in time using interview designed for the purpose. The selection of these six regulatory bodies was made through purposive sampling techniques, in which researcher relies on his or her own judgment when choosing members of the population to participate in the study. The selection of this sampling technique was informed by the objective of the study and the nature of the research question which indicates that participants of these agencies are more relevant in answering the research questions.

3.2 Interview Subjects

The subjects used in conducting the key informants’ interviews (KII) were experts from six FinTech and money laundering related regulatory agencies including CBN, NFIU, EFCC, ICPC, NDLEA and the Ministry of Justice. The use of KII instead of Focus Group Discussion (FGD) form of interviewed has been justified by the nature of research objective which seek to elicit information from specific organization through specific individuals relevant to the subject of the research. Literature documented that KII has been better than FGDs as it provides more in-depth information about the study as it is conducted with individuals that have special knowledge or specific information relating to the research or issue being investigated (Ayegbeli, 2013). Therefore, these justified the deployment of the KII in this study.

This approach is novel in the FinTech and AML literature, which often relies on secondary data or financial institution perspectives. Direct engagement with national regulatory agencies enhances the policy relevance and contextual authenticity of the findings.

3.3 Interview Questions

In line with the objective of the study, thirteen questions were asked to aid the achievement of the objective of the study. These questions were arrived at based on the research objective, reading through the literature as well as preliminary discussion with experts on issues of FinTech and money laundering relevant to the regulatory agencies. This implied that the questions are structured to avoid deviation from the main theme of the study. It also reduced bias in response since the questions and their exact wording are pre-decided, the element of ‘interviewer judgment’ is removed from interviews, leading to consistency in both methodology as well as breadth of information gathered from each participant (Denzin and Lincoln, 1994). These questions are (1) What do you define as “money laundering”? (2) What type of money laundering crimes are prevalent in Nigeria and why? (3) Do you think financial innovation has any effect on money laundering? (4) Aside from digital platforms, what other channels do money launderers use to conceal the source of illicit proceeds? (5) Which digital finance product (ATM, internet banking, POS, and mobile banking) is commonly used for money laundering? (6) Do you think the emergence of cryptocurrency could amplify the effect of financial technology on money laundering? (7) What are the challenges associated with the use of technology in countering money laundering in Nigeria? (8) Are the current laws adequate in curtailing financial technology induced money laundering? (9) Is there any law that specifically focuses on technology-based money laundering? (10) Do you have any partnership with internal and external stakeholders in addressing technology-induced money laundering? (11) How would you describe the effectiveness of those partnerships (if any), (12) Is there any need to strengthen the bilateral and multilateral partnership with your internal and external stakeholders to prevent technology-induced money laundering, and lastly (13) What recommendations would you put in place to prevent financial technology induced money laundering?

3.4 Qualitative Data Analytical Procedure

The qualitative data analysis was conducted using thematic analysis based the five steps identified and recommended by Braun and Clarke (2006). In conducting the analysis, the researchers first familiarized with the data with reading and re-reading, thereafter, transcribed the data and jot down the initial ideas. This was followed initial code generation achieved through writing down small phrase or keywords. These initial codes were read and reread through which identifiable themes were generated for each of the thirteen questions. The themes were subsequently reviewed in such a way to enable the attainment of the research objectives. Lastly, the result is presented with selected vivid and compelling extracts of examples where required. There are justifications for using qualitative analysis especially the application of thematic analysis. Firstly, the nature of the research questions which cannot be answered using quantitative analysis because it is entirely perception of the respondents. Secondly, the dominance of case study methodologies informed the need for exploring alternative methodologies relative to the research questions.

4.0 Results and discussions

In line with the study's objectives, thirteen semi-structured interview questions were posed to key stakeholders across Nigeria's financial regulatory institutions. The responses were analysed using Braun and Clarke's (2006) six-phase thematic analysis approach, which includes: (1) familiarization with the data, (2) generating initial codes, (3) searching for themes, (4) reviewing themes, (5) defining and naming themes, and (6) producing the report.

Figure 3 illustrates the diverse regulatory bodies represented by the study's respondents. This representation underscores the comprehensive nature of the study, capturing a wide array of perspectives on the intersection of FinTech and AML within Nigeria's regulatory landscape.

Figure 3: Nigeria Regulatory Institutions (Respondents)

4.1 Definition and Types of Money Laundering from Regulatory Perspectives in Nigeria

In the literature, money laundering has been defined as illegal process of concealing the source of criminal or illegal proceed by making it appear to have come from a legal business or venture (Odu, 2020). Thus, regulators were asked to define money laundering from their perspectives, several definitions were provided but all revolved around the same meaning as any attempt to make illegally acquired money to appear as if legitimately obtained through manipulating its true source. In this, a respondent from CBN defined the term “money laundering” as:

“Money laundering refers to the process of making illegally obtained money appear legal or legitimate by disguising its true origins. It is a method used by individuals or organizations involved in illegal activities, such as drug trafficking, bribery, fraud, or corruption, to "clean" their proceeds and integrate them into the legal financial system. Money laundering involves several stages, including placement (introducing illicit funds into the financial system), layering (concealing the source or movement of the funds through complex transactions), and integration (making the money available for legal use). The goal of money laundering is to make the illicit funds difficult to trace or detect by authorities (Money Laundering Control Expert – CBN).”

This implied the definitions offered by regulators coincides with those available within the extent of literature, and the respondents have a good understanding of the subject, thus, can be good source of information for the subsequent questions.

Additionally, the respondents were also asked to mention the types of money laundering which are most prevalent in Nigeria and why such happened. They provide several types of money laundering that are prevalent. For instance, a respondent from NDLEA states that:

“Nigeria serves drug trafficking transit point, with the earnings from this unlawful trade frequently subjected to money laundering processes to make them appear legitimate. Money launderers employ diverse strategies, including smuggling cash, establishing shell corporations, and employing layering techniques, to hide the source of proceeds tied to drug-related activities. (Money Laundering Control Experts -NDLEA)”

Therefore, after following the steps of the thematic analysis these were identified as the most common types of money laundering in Nigeria:

Table 4.1: Types of Money Laundering in Nigeria

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Advance fee fraud (commonly known as "419 scams") | This involves enticing victims with promises of large sums of money in exchange for advance fees. The scammers typically use fake identities, emails, or letters to dupe victims into sending money. Once received, the funds are often laundered through complex financial transactions. |

| 2. | Trade-based money laundering | This method involves manipulating trade transactions, such as over- or under-invoicing, to move illicit funds across borders. Criminals may also use fraudulent documents, multiple invoicing, or mispriced goods to disguise the true value of goods being traded. |

| 3. | Public sector corruption | Nigeria has faced significant challenges with corrupt practices in its public sector. Embezzlement, bribery, and kickbacks are common methods through which illicit funds are obtained and subsequently laundered. |

| 4. | Drug trafficking proceeds | Nigeria serves as a transit point for drug trafficking, and the proceeds from this illegal activity are often laundered to legitimize the funds. Money launderers may use various methods, such as cash smuggling, shell companies, or layering techniques, to conceal the origins of drug-related proceeds. |

4.2 Effect of Financial Innovation on Money Laundering

The respondents from the six regulatory agencies were also asked to provide insights into the effect of financial innovation on money laundering. For instance, one of the respondents from EFCC states that:

“ Certainly, financial innovation can indeed influence money laundering. As financial systems and technologies advance, they can have both positive and negative effects on money laundering. On the positive side, innovation can aid in enhancing compliance measures and regulatory frameworks. Technologies like AI and machine learning can be used to analyze vast financial data, identify patterns, and detect suspicious transactions more efficiently. However, from a negative standpoint, criminals can exploit emerging financial technologies for money laundering. Innovations like digital currencies, such as cryptocurrencies, offer anonymity and enable cross-border transfers, complicating efforts by authorities to track and uncover illicit funds (Money Laundering Control Expert -EFCC). ”

Therefore, observing the steps of thematic analysis, the following themes have been identified from both positive and negative viewpoints:

Table 4.2: Effects of Financial Innovation on Money Laundering

| S/N | Themes | Explanation |

|---|---|---|

| Negative Effects of FinTech on Money Laundering | ||

| 1. | Enhanced Compliance Measures | Financial innovation can facilitate the development of improved compliance measures and regulatory frameworks. Advanced technologies, such as artificial intelligence and machine learning, can be leveraged to analyze large amounts of financial data, identify patterns, and detect suspicious transactions more effectively. |

| 2. | Improved Transparency | Innovations like blockchain technology can enhance transparency and traceability in financial transactions. The immutable nature of blockchain records can make it more difficult for criminals to conceal their illicit activities and launder money. |

| Negative Effects of FinTech on Money Laundering | Meaning | |

| 1. | Exploitation of New Channels | Criminals can exploit emerging financial technologies to further their money laundering operations. Innovations like digital currencies (e.g., cryptocurrencies) can provide anonymity and facilitate cross-border transfers, making it challenging for authorities to trace and identify illicit funds. |

| 2. | Complexity in Financial Structures | Financial innovations can introduce complex financial structures and instruments that can be used to obscure the true origins of funds. Criminals may use techniques such as layering, smurfing, shell companies, or complex cross-border transactions to launder money more effectively. |

Therefore, these findings could be supported by the postulation of Technological Determinism Theory (McLuhan, 1964) which highlights the link between FinTech and money laundering exposure. Thus, the theoretical insights from Technological Determinism Theory (McLuhan, 1964) is consistent with both positive and negative links between FinTech and money laundering found in this study.

4.3 Non-Digital Platforms Use by Money Launders to Conceal Source of Illicit Proceeds

The respondents were also asked to state other various channels apart from digital platforms used by money launderers to hide the source of illicit proceeds in which they mentioned several other channels. For instance, an expert from ICPC explained that:

“ Besides digital platforms, money launderers can employ diverse channels to obscure the origin of illegal proceeds. This may involve investing in high-value properties or real estate ventures to transform illicit funds into seemingly lawful assets. Properties can be subjected to multiple transactions, creating layers of complexity, and obfuscating the funds' true source. (Money laundering Control Experts – ICPC) ”

Upon applying the steps of thematic analysis, the following themes have been identified as follows:

Table 4.3: Non-Digital Platforms Use by Money Launders to Conceal Source of Illicit Proceeds

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Cash-intensive businesses | Money launderers may operate businesses that deal primarily in cash to co-mingle illegal funds with legitimate revenue. Examples include casinos, restaurants, nightclubs, or retail stores where large sums of cash transactions are common. |

| 2. | Real estate investments | Money launderers may invest in high-value properties or real estate projects to convert illicit funds into seemingly legitimate assets. Properties can be bought and sold multiple times to layer and obscure the source of the funds. |

| 3. | Offshore accounts and tax havens | Money launderers may use offshore accounts and tax havens that offer strict banking secrecy laws and limited transparency. These jurisdictions make it challenging for authorities to trace the illicit funds back to their source. |

| 4. | Trade misinvoicing | Criminals may manipulate trade transactions by over- or under-invoicing goods or services to move money across borders without raising suspicion. This involves the use of fraudulent invoices and misrepresentation of the value or quantity of traded goods. |

| 5 | Shell companies | Money launderers may set up shell companies, which exist only on paper and have no legitimate business operations, to disguise the true ownership and purpose of the funds. These entities can be used to conduct transactions that appear legitimate but are moving illicit funds. |

| 6 | Smurfing | Also known as structuring, smurfing involves breaking up large sums of money into smaller, less noticeable transactions to avoid suspicion. Money launderers may use multiple individuals or accounts to make multiple deposits or transfers below reporting thresholds, making it harder for authorities to detect the illegal activity. |

4.4 Most Common Digital Finance Product (ATM, Internet Banking, POS, Mobile Banking, etc.) Deployed for Money Laundering

With respect to the question on the most common digital finance products (ATM, Internet Banking, POS, Mobile Banking, etc.) being used by money launderers in committing crime, it was found that any digital finance product can potentially be utilized for money laundering, depending on the specific circumstances and the methods employed by criminals. In this, a respondent from NFIU states that:

“Any digital financial product has the potential for money laundering use, depending on circumstances and criminal tactics. Nevertheless, some digital finance products are more frequently linked to money laundering due to their convenience and potential for anonymity. For example, online payment platforms like e-wallets and peer-to-peer services offer fast, convenient fund transfers, enabling criminals to move illicit funds between accounts or conduct anonymous transactions. (Money Laundering Control Expert – NFIU)”

Further analysis of the data from the six respondents using thematic analysis, the following themes have been identified which served as the most common digital financial products used for money laundering in Nigeria, which is consistent with the postulation of Technological Determinism Theory (McLuhan, 1964) which highlights that FinTech influences money laundering:

Table 4.4: Most Common Digital Finance Product (ATM, Internet Banking, POS, Mobile Banking, etc) Deployed for Money Laundering

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Cryptocurrencies and virtual currencies | These digital currencies, which operate on decentralized networks and often offer a degree of anonymity, have been associated with money laundering activities due to the difficulty in tracing transactions and identifying the true owners of funds. |

| 2. | Online payment platforms | These platforms, such as e-wallets or peer-to-peer payment services, provide quick and convenient methods for transferring funds. Criminals may utilize these platforms to move illicit funds between accounts or make anonymous transactions. |

| 3. | Online payment platforms | These platforms, such as e-wallets or peer-to-peer payment services, provide quick and convenient methods for transferring funds. Criminals may utilize these platforms to move illicit funds between accounts or make anonymous transactions. |

| 4. | Digital remittance services | These services allow individuals to send money electronically across borders. Criminals may exploit these services to transfer illicit funds, taking advantage of the speed and potential lack of proper identification or due diligence measures. |

| 5 | Online banking | While internet banking itself is not inherently used for money laundering, criminals may leverage it as a means to transfer funds between accounts or conduct fraudulent transactions, particularly if they have gained unauthorized access to someone's online banking credentials. |

4.5 Increasing Effect of Financial Technology on Money Laundering through Emergence of Cryptocurrency

The respondents were asked whether the emergence of cryptocurrency has amplified the effects of FinTech on money laundering. They responded that the emergence of cryptocurrency has indeed introduced new opportunities and challenges with respect to money laundering. While cryptocurrencies offer various benefits such as decentralized networks and faster transactions, they also present certain characteristics that can be exploited by money launderers. For instance, a respondent from NFIU revealed that:

“The rise of cryptocurrency has brought forth both fresh prospects and challenges in the realm of money laundering. Cryptocurrencies provide decentralized networks and swift transactions, but they also harbor traits susceptible to exploitation by money launderers, primarily anonymity. Cryptocurrency transactions employ pseudonyms, making it difficult to ascertain the real identities involved, a feature that can be alluring to money launderers (Money Laundering Control Expert -NFIU)”

Further analysis of the responses from experts in money laundering and FinTech related regulatory agencies revealed the following themes in relation to why the emergence of cryptocurrency amplified the effect of FinTech on money laundering:

Table 4.5: Increasing Effect of Financial Technology on Money Laundering through Emergence of Cryptocurrency

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Anonymity | Cryptocurrencies can provide a certain level of anonymity as transactions are conducted using pseudonyms, making it challenging to identify the real-world identities behind the transactions. This anonymity can be attractive to money launderers. |

| 2. | Borderless Transactions | Cryptocurrencies enable borderless transactions without the need for intermediary financial institutions. This feature can make it easier for money launderers to move funds across borders quickly and discretely. |

| 3. | Lack of Regulation | The regulatory frameworks around cryptocurrencies are constantly evolving, and in some jurisdictions, they are still developing. This can create gaps and loopholes that money launderers may exploit. |

| 4. | Tumbling and Mixing Services | Money launderers use tumbling and mixing services to further obfuscate the source of cryptocurrency transactions. These services break up transactions into smaller parts, mix them with other transactions, and redistribute funds to hinder traceability. |

However, it is important to note that the increased usage of cryptocurrencies has also prompted significant efforts by regulators, governments, and financial institutions to address the risks associated with money laundering. Many jurisdictions have implemented or are developing regulations to require cryptocurrency exchanges and service providers to implement anti-money laundering measures and conduct proper customer due diligence. Furthermore, advancements in blockchain analysis and forensic technologies are being utilized to trace illicit transactions and identify patterns associated with money laundering activities within the cryptocurrency space, this confirmed the postulation of Technological Determinism Theory (McLuhan, 1964) that FinTech influences money laundering exposure. Collaborative efforts between the private and public sectors are continuously evolving to enhance the transparency and integrity of cryptocurrency transactions.

4.6 Challenges Associated with the Application of Technology in Countering Money Laundering in Nigeria

In relation to this, the respondents revealed that the use of technology to counter money laundering in Nigeria faces several challenges. For instance, a respondent from CBN disclosed that:

“ One of the significant challenges is an ever-changing regulatory environment which lies in the constant evolution of the regulatory landscape for technology and anti-money laundering measures. Adapting current regulations to incorporate new technologies and digital platforms, while maintaining effective oversight, presents challenges and necessitates close collaboration between regulatory bodies, financial institutions, and technology providers. (Money Laundering Control Expert – CBN)”

Further analysis of the responses from experts in the six regulatory agencies using the steps in thematic analysis enabled the identification of the themes relating to the challenges Associated with the Application of Technology in Countering Money Laundering in Nigeria, which include:

Table 4.6: Challenges Associated with the Application of Technology in Countering Money Laundering in Nigeria

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Limited Technology Infrastructure | Adequate technology infrastructure, including reliable internet connectivity and digital infrastructure, is essential for effective implementation of anti-money laundering measures. In regions with limited technology infrastructure in Nigeria, the adoption and implementation of advanced technological solutions can be hindered. |

| 2. | Digital Divide | Nigeria has a significant digital divide, with a large portion of the population lacking access to digital platforms and technology. This can make it harder to implement and enforce digital-based anti-money laundering measures, as criminals may exploit gaps in technology adoption. |

| 3. | Lack of Awareness and Training | Insufficient awareness and training on technology-based anti-money laundering measures can hinder their effective implementation. Both financial institutions and law enforcement agencies may lack the necessary expertise and knowledge to effectively leverage technology in combating money laundering. |

| 4. | Evolving Techniques and Sophisticated Criminals | Money launderers continually adapt their techniques to exploit vulnerabilities in technology-based systems. They may employ advanced encryption methods, utilize dark web platforms, or employ other sophisticated techniques to evade detection. Law enforcement agencies and institutions must stay updated and continually evolve their technological capabilities to keep pace with these changing tactics. |

| 5 | Dynamic Regulatory Environment | The regulatory landscape for technology and anti-money laundering measures is constantly evolving. Adapting existing regulations to accommodate new technologies and digital platforms, while ensuring robust oversight, can be challenging and may require strong collaborations between regulatory bodies, financial institutions, and technology providers. |

| 6 | Cross-Border Challenges | Money laundering often involves cross-border transactions, which require international cooperation and coordination between jurisdictions. Different countries may have varying technological capabilities, regulatory frameworks, and levels of cooperation, making cross-border investigations and enforcement complex. |

Some of these techniques that could be applied in countering money laundering are technology related, thus, implying the link between FinTech and money laundering in line with the postulation of Technological Determinism Theory (McLuhan, 1964).

4.7 Adequacy of the Current Laws in Curtailing Financial Technology Induced Money Laundering and the need for Specific Laws on Technology-based Money Laundering

In relation to this, it was found that in Nigeria, efforts have been made to develop and implement laws and regulations to address money laundering, including that which occurs through financial technology. With respect to this, a respondent from Ministry of Justice and CBN revealed that:

“The primary legislation governing anti-money laundering efforts in Nigeria is the Money Laundering (Prohibition) Act 2011 (as amended in 2012), along with other related regulations issued by the Central Bank of Nigeria (CBN) and the Economic and Financial Crimes Commission (EFCC). However, the adequacy of these laws in curtailing financial technology-induced money laundering can vary depending on several factors (Money Laundering Law Expert – Ministry of Justice).

“The CBN has issued guidelines on the use of financial technology and Anti-Money Laundering Regulation in Nigeria. (Money Laundering Control Expert – CBN)”

Further analysis of the responses using thematic analysis revealed that, in Nigeria like in most jurisdictions, the rapid advancements in financial technology present ongoing challenges for regulatory frameworks. Some potential areas where the current laws in Nigeria may face challenges in curtailing financial technology-induced money laundering include:

Table 4.7: Some potential areas where the current laws in Nigeria may face challenges in curtailing financial technology-induced money laundering

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Cryptocurrencies | The laws in Nigeria do not provide specific regulations for cryptocurrencies. This can create challenges in effectively addressing the risks associated with cryptocurrency-based money laundering. |

| 2. | Digital Identity Verification | Adequate digital identity verification plays a crucial role in combating money laundering. However, there may be challenges related to the implementation and enforcement of standardized digital identity verification processes in the Nigerian financial ecosystem. |

| 3. | Cross-Border Transactions | Money laundering often involves cross-border transactions, which require international cooperation. Although Nigeria has entered into various agreements to enhance international collaboration, challenges related to jurisdictional constraints and differences in regulatory frameworks may still exist. |

| 4. | Ongoing Technological Advancements | The rapid pace of technological advancements necessitates continuous adaptation of laws and regulations to keep pace with emerging money laundering risks and innovative methods employed by criminals |

It is important to note that to address these challenges, Nigerian authorities have been enhancing their efforts, including ongoing collaborations with international bodies and organizations, to strengthen the legal and regulatory frameworks. This includes ongoing amendments to laws and the development of specific regulations related to financial technology and money laundering. Moreover, it can be deduced that the effectiveness of laws and regulations in curtailing financial technology-induced money laundering also depends on the enforcement efforts, capacity building, and coordination among different stakeholders, including financial institutions, regulatory bodies, and law enforcement agencies.

Furthermore, the respondents were also asked whether there is specific laws designed exclusively to address technology-based money laundering, however, it was found that such laws do not exist in the country. On this, an expert in money laundering law from Ministry of Justice and expert from CBN revealed that:

“In Nigeria, there is no specific law that exclusively focuses on technology-based money laundering. However, existing laws and regulations, such as the Money Laundering (Prohibition) Act 2011 (as amended in 2012). The Money Laundering Act prohibits money laundering activities regardless of the means used to commit the offense. It encompasses all forms of money laundering, including those that involve financial technology. The Act imposes obligations on financial institutions, including banks and other designated non-financial institutions, to implement anti-money laundering measures and report suspicious transactions. (Money Laundering Law Expert – Ministry of Justice)”

“The guidelines issued by the Central Bank of Nigeria (CBN), encompass various forms of money laundering, including those facilitated by technology. These guidelines address the use of technology in financial transactions and emphasize the importance of adopting appropriate anti-money laundering measures in the digital context. These guidelines outline requirements and expectations for financial institutions to combat money laundering using technology channels. (Money Laundering Control Expert – CBN)”

Therefore, it can be concluded there that while there is no specific law dedicated solely to technology-based money laundering, the existing laws and regulations are intended to be comprehensive and adaptable enough to address money laundering risks, including those arising from advancements in financial technology. However, it is essential for regulators and authorities to continuously assess and update these laws in response to emerging risks and technological developments or to design specific laws relating to technology-induced money laundering.

4.8 Partnership with Internal and External Stakeholders in Addressing Technology-induced Money Laundering

The regulators were asked to give perspectives on whether partnership with internal and external stakeholders help in addressing technology-induced money laundering. One of the respondents from NFIU explained that:

“ Nigeria has taken steps to combat tech-based money laundering through internal and external partnerships. Domestically, institutions like the EFCC and NFIU work to prevent money laundering via technology. Nigeria also collaborates with the private sector, including banks and FinTech firms, to bolster anti-money laundering efforts and secure digital transactions, reducing tech-related laundering risks. Nigeria has established international collaborations in its fight against money laundering. As a member of the Egmont Group, a global network of financial intelligence units, Nigeria shares information and combats money laundering, including tech-related cases, across borders. The country also partners with international bodies like FATF and UNODC to create and enforce anti-money laundering measures, especially those pertaining to technology-driven laundering . (Money Laundering Control Expert – NFIU)”

Analyzing the responses from all the respondents through thematic analysis established two themes of partnerships, which are internal and external collaborations.

Table 4.8: Areas of Partnership with Internal and External Stakeholders in Addressing Technology-induced Money Laundering

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Internal Collaboration | Internally, the Nigerian government has established institutions and regulatory bodies such as the Economic and Financial Crimes Commission (EFCC) and the Nigerian Financial Intelligence Unit (NFIU). These agencies work towards preventing money laundering and illicit financial activities, including those conducted through technology platforms. Additionally, Nigeria has engaged with the private sector, including banks, FinTech companies, and technology service providers, to establish robust anti-money laundering measures. These collaborations aim to enhance the security and integrity of digital financial transactions, thereby reducing the risk of technology-induced money laundering. |

| 2. | External/International Collaboration | Nigeria has also forged international partnerships to combat money laundering. The country is a member of the Egmont Group, which is a global network of financial intelligence units that collaborates to share information and combat money laundering and terrorist financing. This membership allows Nigeria to exchange information with other countries to investigate and prevent money laundering, including those related to technology. Furthermore, Nigeria collaborates with international organizations such as the Financial Action Task Force (FATF) and the United Nations Office on Drugs and Crime (UNODC). These partnerships help Nigeria develop and implement anti-money laundering measures, including those specific to technology-induced money laundering. |

Overall, the regulatory agencies in Nigeria acknowledge the importance of partnerships with both internal and external stakeholders in addressing technology-induced money laundering. These collaborations help strengthen the country's capacity to combat money laundering through technological platforms and protect its financial system.

Additionally, the respondents were also asked to offer some insights about the effectiveness of these internal and external collaborations. In this, a respondent from NFIU offers the following insights:

“ Partnerships in Nigeria have been highly effective in addressing technology-induced money laundering. Agencies such as NFIU and EFCC play key roles in investigating and prosecuting financial crimes, including those involving technology. Nigeria's affiliation with the Egmont Group provides access to crucial information networks, strengthening investigative capabilities and global cooperation against money laundering. This partnership aids Nigeria in preventing money laundering, especially via technology platforms. Collaborations with the private sector allow the implementation of KYC and AML compliance programs, enhancing the detection and prevention of illicit financial activities through technology platforms. (Money Laundering Control Expert – NFIU)”

However, thematic analysis of the responses from all the agencies revealed that while these partnerships demonstrate Nigeria's commitment to addressing technology-induced money laundering, the effectiveness of these collaborations can vary depending on various factors, which are discussed in the following themes:

-

Level of Information Sharing: openness of the partners in sharing vital information determines the effectiveness of the partnership, where vital information are conceal the aim of the partnerships may not be achieved irrespective of the number of partnerships entered into.

-

Resources: where resources allocated to the implementation of the partnership are not adequate, the effectiveness of the partnerships will be questionable.

-

Capacity to implement and enforce regulations: the capacity of the collaborating agencies in the implementation and enforcement of the partnership also determine its effectiveness, where such are lacking, the partnership will be ineffective.

-

Continual Assessment and Evaluation: Continual assessment and evaluation of the internal and external partnership is a significant factor in determining their effectiveness. This can be achieved through withdrawing from obsolete ones, maintaining effective ones and exploring new opportunities for fruitful partnership.

4.9 Strengthening Bilateral and Multilateral Partnership to Prevent Technology-induced Money Laundering

The respondents were asked whether strengthening bilateral and multilateral partnerships have potentials to effectively prevent technology-induced money laundering. In this, a respondent gave an insight from NFIU, viz:

“ Enhancing both bilateral and multilateral partnerships with Nigeria's internal and external collaborators is imperative to combat technology-induced money laundering effectively. Strengthening ties with external stakeholders facilitates the alignment of legal frameworks and regulatory standards, closing potential loopholes that tech-savvy money launderers could exploit. This coordinated effort contributes to establishing a coherent and resilient global framework for tackling technology-driven money laundering. (Money Laundering Control Expert -NFIU) ”

Further thematic analysis across the responses from the regulatory agencies revealed important themes with respect to impact of strengthening bilateral and multilateral partnerships on effective prevention of technology-induced money laundering as analyzed below:

Table 4.9: Strengthening Bilateral and Multilateral Partnership to Prevent Technology-induced Money Laundering

| S/N | Themes | Explanation |

|---|---|---|

| 1. | Enhanced Information Sharing | Bilateral and multilateral partnerships can facilitate the exchange of information and intelligence between Nigeria and other countries. This collaboration is crucial in identifying cross-border money laundering activities conducted through technology platforms and coordinating efforts to prevent such illicit financial flows. |

| 2. | Harmonization of Legal Frameworks | Strengthening partnerships with external stakeholders allows for the harmonization of legal frameworks and regulatory standards. This alignment helps ensure that there are no loopholes that can be exploited by money launderers using technology. It enables the creation of a consistent and robust global framework to combat technology-induced money laundering. |

| 3. | Capacity Building | Partnering with external stakeholders provides opportunities for capacity building initiatives. Nigeria can benefit from technical assistance, training programs, and knowledge sharing from more advanced jurisdictions. These initiatives can enhance the capabilities of Nigerian institutions and stakeholders in combating technology-induced money laundering. |

| 4. | International Cooperation in Investigations | Bilateral and multilateral partnerships enable greater cooperation between law enforcement agencies and regulatory bodies across jurisdictions. This cooperation is vital in investigating and prosecuting complex cases of technology-induced money laundering that involve multiple countries or jurisdictions. |

| 5. | Access to Technical Expertise | Collaborating with external stakeholders can give Nigeria access to technical expertise and innovative solutions in the field of financial technology and anti-money laundering. This knowledge transfer can help Nigeria stay abreast of advancements in technology and develop effective measures to counter emerging risks. |

| 6 | Promoting Confidence in the Financial System | Strong partnerships with external stakeholders contribute to building trust and confidence in Nigeria's financial system. This improves Nigeria's reputation as a responsible and secure financial hub, attracting foreign investment and fostering economic growth. |

Overall, strengthening bilateral and multilateral partnerships with both internal and external stakeholders is essential for Nigeria to effectively prevent technology-induced money laundering. It allows for improved information sharing, harmonized legal frameworks, enhanced capacity, international cooperation, and access to technical expertise, all of which are crucial in combating this global financial crime.

4.10 Recommendations for Prevention of FinTech induced Money Laundering

The respondent from regulatory agencies were also asked to offer some recommendations with respect to the prevention of financial technology-induced money laundering. Several recommendations were made in this regard. For instance, respondent from Ministry of Justice recommended that:

“To fortify the legal and regulatory framework, it's crucial to update existing laws and regulations, specifically targeting the risks associated with financial technology-induced money laundering. This entails incorporating provisions for robust customer due diligence, comprehensive transaction monitoring, and mandatory reporting of suspicious activities. These updates are essential for staying ahead of evolving financial technologies and effectively countering money laundering. (Money Laundering Law Expert – Ministry of Justice)”

Furthermore, thematic analysis of the recommendation from all the participating experts in the interview revealed some interesting themes of policy recommendation as shown in the following:

-

Strengthen Regulatory Framework: Enhance the legal and regulatory framework by updating existing laws and regulations to address the specific risks posed by financial technology-induced money laundering. This should include provisions for customer due diligence, transaction monitoring, and reporting suspicious activities.

-

Collaboration and Information Sharing: Foster collaboration and information sharing between regulatory bodies, law enforcement agencies, financial institutions, and technology service providers. This includes establishing platforms for sharing information, intelligence, and best practices to identify emerging money laundering trends related to financial technology.

-

Enhance Customer Due Diligence: Implement robust Know Your Customer (KYC) procedures for financial institutions and technology service providers. This includes verifying the identity of individuals or entities involved in transactions and assessing their risk profiles. Utilize digital identity verification technologies to strengthen the accuracy and efficiency of the KYC process.

-

Implement Transaction Monitoring: Develop and enforce effective transaction monitoring systems to detect suspicious activities conducted through financial technology platforms. Utilize advanced analytics, machine learning, and artificial intelligence techniques to identify patterns and anomalies indicative of money laundering.

-

Training and Awareness Programs: Conduct regular training and awareness programs for financial institutions, technology service providers, and relevant stakeholders to educate them about the risks of financial technology-induced money laundering. This will help improve their understanding of red flags, reporting obligations, and the importance of compliance with anti-money laundering regulations.

-

International Cooperation: Strengthen international cooperation and collaboration with other countries and international organizations to counter cross-border financial technology-induced money laundering. This includes sharing intelligence, harmonizing regulatory frameworks, and aligning efforts in combating this global issue.

-

Continuous Monitoring and Evaluation: Regularly monitor and evaluate the effectiveness of preventive measures and partnerships in addressing financial technology-induced money laundering. Periodic assessments will help identify areas of improvement, keep pace with evolving threats, and ensure the implementation of adequate preventive measures.

Therefore, it is unarguable that by implementing these recommendations, Nigeria can enhance its ability to prevent financial technology-induced money laundering and protect its financial system from illicit activities.

5.0 Conclusions and implications

The paper seeks to explore the perception of regulators on the issues of FinTech and money laundering in Nigeria. This has been attained through interviews with key informants in six FinTech and money laundering regulatory bodies in Nigeria. The outcome of the interview revealed that revealed several types of money laundering that are prevalent in Nigeria, and financial innovation could have both positive and negative effect on money laundering. Moreover, in addition to digital platforms, money launderers deployed non-technology-based channels in perpetuating their money laundering activities in Nigeria. However, with respect to digital platforms, any can be utilized for money laundering depending on the circumstance, with cryptocurrency introducing new opportunities and challenges with respect to money laundering. It was also found that use of technology to counter money laundering in Nigeria faces several challenges, and while effort have been made to develop and implement laws and regulations to address money laundering, there is no specific law that exclusively focuses on technology-based money laundering. Lastly, partnerships with both internal and external stakeholders can be assist in addressing technology-induced money laundering, although its effectiveness depends on different factors, consistent with these the regulators offered some recommendations to prevent financial technology-induced money laundering through strengthen bilateral and multilateral partnerships with Nigeria's internal and external stakeholders.

5.1 Theoretical Contributions

This study makes a significant contribution by advancing the application of Technological Determinism Theory within the context of financial technology and anti-money laundering (AML) regulation. While prior research such as Hariyono and Tjahjadi (2021) has begun to explore this theoretical lens in FinTech, its use remains limited. This study extends the theory in three important ways: (1) by applying it to the regulatory domain, (2) by empirically examining how technological features shape institutional responses, and (3) by contextualizing these dynamics within a developing country setting. Specifically, the study operationalizes Technological Determinism by demonstrating how core FinTech attributes such as decentralization, anonymity, and cross-border capability pose structural constraints on regulatory oversight. This reinforces McLuhan’s central thesis that “the medium shapes the environment,” in this case, highlighting how FinTech technologies influence the architecture and effectiveness of regulatory frameworks. In doing so, the study not only enriches the theoretical discourse but also contributes to the global AML/CFT literature by offering insights from Nigeria Africa’s largest economy on the intersection between financial innovation and illicit finance exposure.

5.2 Policy Recommendations

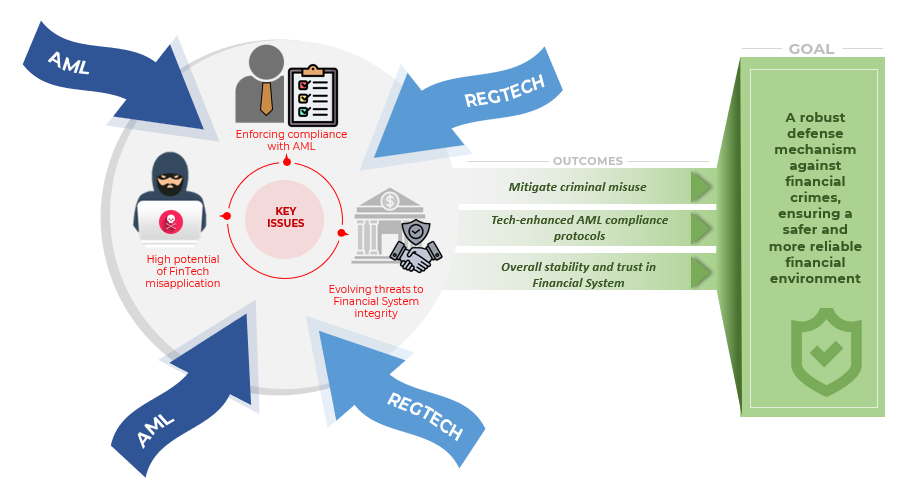

In terms of policymaking, the study provides specific recommendations to enhance the use of FinTech and mitigate money laundering in Nigeria as well as global AML/CFT practitioners and implications for practice. Firstly, within the global space, the finding of the study contributes to the global AML/CFT practitioners in understanding different dynamics and roles of FinTech in fueling and sometimes countering money laundering since it was found to have both positive and negative effect on money laundering exposure. Secondly, the study suggests that higher regulatory quality is associated with a strengthened relationship between FinTech and money laundering. Given the increased risk of money laundering with higher FinTech usage, stringent financial regulations can reduce the impact of FinTech on money laundering exposure in Nigeria. The research findings recommend for robust regulatory interventions in addressing money laundering risks associated with emerging financial technologies, encompassing the evolving landscape of cash and payment infrastructure, cryptocurrencies, and central bank digital currency infrastructure. Figure 4 illustrates the pivotal role of RegTech in bridging AML/CFT measures with FinTech regulations, reinforcing the study’s call for technology-oriented regulatory interventions. By proactively mitigating financial crime risks, RegTech solutions facilitate a well-regulated exchange between FinTech and central banks, ensuring compliance while paving the way for a resilient and innovative digital payment infrastructure.

Figure 4: Address potential Risks and improve resilience (Source Author Creation)

The Central Bank of Nigeria is encouraged to not only design relevant regulations but also collaborate with financial law enforcement agencies, such as the Economic and Financial Crimes Commission, the Independent Corrupt Practices and Other Related Offences Commission, and the Nigerian Financial Intelligence Unit, to ensure effective implementation.

Thirdly, the study emphasizes the opportunity provided by Nigeria's legal system (both civil and common laws) to ring-fence electronic fund transactions. Ring-fencing electronic funds can prevent commingling with other assets, offering protection against claims by other creditors, even in cases of insolvency. This measure can reduce the likelihood of money laundering, especially when electronic funds are often used for settling obligations or conducting illicit transactions.

Fourthly, the Central Bank of Nigeria is urged to make substantial investments in financial infrastructure to address the growing disparity in financial system development. Closing the gap in financial infrastructure within the country, between urban and rural areas, and between Nigeria and other emerging countries could potentially stabilize the impact of FinTech on money laundering, particularly when coupled with effective regulations and enhanced financial literacy.

Lastly, the findings of the study could be beneficial to the global banking industry, especially among the FinTech companies and central banks. In this, much could be learnt with respect to the types of money laundering, effects of FinTech on money laundering, areas where new laws relating to FinTech and money laundering could be enacted as well as the importance of internal and external collaborations in curtailing the effect of FinTech on money laundering. In specifics, the findings could be of relevance to IMF, FAFT, GIABA among other relevant organizations.

Key Contributions:

-

Offers first-hand insights from six Nigerian regulatory institutions on FinTech-induced money laundering.

-

Applies Technological Determinism Theory in a regulatory and AML context, rarely done in existing literature.

-

Reveals critical gaps in cryptocurrency legislation and enforcement frameworks.

-

Provides a detailed thematic breakdown of institutional responses, risks, and partnership dynamics.

While focused on Nigeria, the study's findings offer valuable lessons for other emerging markets grappling with similar issues. It underscores the importance of contextualized regulatory capacity, multi-level partnerships, and technology-responsive legal reform principles applicable across FinTech-intensive jurisdictions globally.

5.3 Limitation and Direction for Future Research

Despite that the study achieved its objectives, it is associated with some limitations which serve as justifications for further research. First, the small number of samples from only six regulatory agencies, though is sufficient for our purpose, nevertheless it implied the need for larger samples especially from countries with larger numbers of regulatory agencies beyond Nigeria. Secondly, the qualitative method deployed in this study is cross-sectional with opinions and perceptions expressed being timebound. Hence, the need for future studies to explore the application of time series data to test the sustainability of these findings overtime. Lastly, the study covers only Nigeria, although it is the largest country within Africa, there still a need for more studies either in other countries or comparative studies across countries.

References

Alexandre, C. R., & da Silva, J. B. (2023). Incorporating machine learning and a risk-based strategy in an anti-money laundering multiagent system. Expert Systems with Applications , Vol. 217, 119500. https://doi.org/10.1016/j.eswa.2023.119500

Alexandre, C.R. and da Silva, J.B., 2023. Incorporating machine learning and a risk-based strategy in an anti-money laundering multiagent system . Expert Systems with Applications, 217, p.119500. https://doi.org/10.1016/j.eswa.2023.119500

Ali, Y., 2019. FinTech and Money Laundering: A Case Study Approach . Journal of Financial Crime, 26(3), pp.789–803.

Ayegbile, D. (2013). Interviews & Focus Group Discussions . https://pilafui.org/wp-content/uploads/2021/02/PiLAFs-Interviews-Focus-Group-Discussions.pdf

Bhunia, A et al. (eds.) (2023). Proceedings of the 2023 International Conference on Finance, Trade and Business Management (FTBM 2023), Advances in Economics, Business and Management Research 264 , https://doi.org/10.2991/978-94-6463-298-9_20

Bjelajac, Ž. Đ. (2011). Contemporary tendencies in money laundering methods: review of the methods and measures for its suppression. Research Institute for European and American Studies .

Bodescu, C. N., Achimb, M. V., & Rusc, A. I. D. (2022). The influence of digital technology in combating money laundering. In 24th RSEP International Conference on Economics, Finance & Business– Virtual/Online 24-25 February 2022.

Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative research in psychology, 3(2), 77-101.

Campbell-Verduyn M. (2018) Bitcoin, crypto-coins, and global anti-money laundering governance, Journal of Crime, Law and Social Change 69 (1)

CBN (2018). Anti-money Laundering and Combating Financial Terrorism (Administrative Sanction) Regulation, 2018. Available online at: https://www.cbn.gov.ng/Out/2018/FPRD/Administrative%20Sanction%20Regime.pdf. Accessed 23rd November 2021

Denzin, N. K., & Lincoln, Y. S. (1995). Transforming qualitative research methods: Is it a revolution? Journal of Contemporary Ethnography , 24(3), 349-358.

Financial Action Task Force (FATF), 2023. Opportunities and Challenges of Emerging Technologies for AML/CFT . [online] Available at: https://www.fatf-gafi.org [Accessed 7 May 2025].

Financial Action Task Force (FATF), 2024. Nigeria's progress in measures to combat money laundering and terrorist financing . [online] FATF. Available at: https://www.fatf-gafi.org/en/publications/Mutualevaluations/Nigeria-FUR-2024.html [Accessed 7 May 2025].

Financial Crime Academy (2023) The Three Stages of Money Laundering and How Money Laundering Works Available online https://financialcrimeacademy.org/the-three-stages-of-money-laundering/ Accessed 24 th January 2024

FSB (2023) Financial Innovation and Structural Change Available online at https://www.fsb.org/work-of-the-fsb/financial-innovation-and-structuralchange/fintech/#:~:text=The%20FSB%20defines%20FinTech%20as,the%20provision%20of%20financial%20services . Accessed 22nd January 2024